Private sector debt in Scotland – the real ticking time bomb

You can be sure of one thing. If politicians and mainstream economists are not talking about something, it must be important. We live in an era of misdirection. Ample headlines and column inches are dedicated to the national debt. Nothing is written about private sector debt.

Thankfully, both Professor Richard Murphy and Professor Steve Keen have been keeping this topic bubbling over for the last while (for Steve Keen, it has pretty much been his life’s work). The same can not be said of the economic mainstream.

The mainstream framing that public debt is the problem belies the evidence

In mature Western nation-states, such as the UK, financial crises are most often caused by private sector debt. They are very rarely caused by sovereign debt.

Greece, perhaps surprisingly, provides some solid evidence.

After the financial crisis in 2008, the European Central Bank refused to act as the lender of last resort, and the Greek economy suffered (its GDP is still 20% lower than in 2008!). However, by 2012, the ECB’s position had changed, and it announced that it would do ‘whatever it takes’ to stabilise the Euro. This, in effect, backstopped all Greek government debt. Suddenly, Greece’s public debt was not a problem.

As you can see, the issue (public debt in 2011 was roughly the same as the debt level today) remains, but the problem has disappeared. And all because the ECB now does its job.

As long as a nation has a central bank that can purchase government debt, issued in the country’s own currency*, it can never go bust. The simple reason is that, as the creator of the currency, it can always pay interest on its debt.

The same, of course, can not be said about the private sector.

Facing demands to pay off debt, a company, household, or individual must be able to earn or borrow to pay off their debt; there is no option available to the private sector to create the unit of account that will clear their debt, that privilege lies only with the State (the UK).

*The Euro is unique, but the result is the same.

There are other reasons why public debt is a much less significant issue than private debt

The state has vast resources and significant assets. It can always liquidate assets if it decides to fund debt repayments from another source. It is also backed by ‘the violence of the state’; the government can seize your bank account, fine you for all manner of things, and increase taxes. Government debt will always be repaid.

And of course, perhaps the most overlooked fact is that the government sets the interest rate on its liabilities.

At the next meeting of the Bank of England’s Monetary Policy Committee, an announcement could be made that the current rate (4% as of September 2025) was reduced to 1%. Or 0%.

Immediately, the interest on government liabilities – newly created debt, and reserve balances at the Bank of England would drop to 1%. And billions of pounds would be saved each year.

If only each individual in the private sector had that option!

What do Scotland’s sectoral balances tell us about private sector debt in Scotland

Here are Scotland’s sectoral balances that show the net saving position for three sectors of the economy. You can see a detailed explainer on Scotland’s sectoral balances here.

Let’s focus on the blue bar—the private sector balance. When it is above the zero line, the private sector has been able to net save. When it is below, it is spending more than it earns, which is the source of financial instability.

Scotland’s Historic Sectoral Balances

These sectoral balances don’t reveal who within the private sector is net saving (it is made up of households, the financial services sector, and the non-financial corporate sector), but they provide insight into the ‘debt stress’ of the private sector as a whole.

It presents a very worrying picture. In only seven out of the twenty-five years has the Scottish private sector been able to ‘net save’. We, of course, intuitively know who feels the pain the most: the already debt-stressed.

The lowest-earning 50% of Scots have seen stagnant income over the last decade and a half. Meanwhile, the cost of living has continued to rise. People are going without essentials. And debt is financing the gap.

Private sector debt in Scotland

Private sector debt is a significant concern, particularly in Scotland.

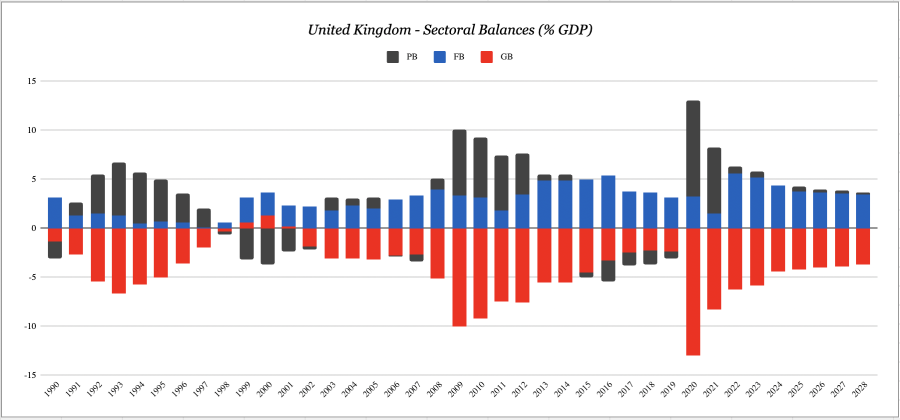

Below is the UK’s sectoral balances. And you will see that over the last twenty-five years, the UK private sector as a whole has been able to ‘net save’ in fourteen years, twice as often as the Scottish private sector. This is clear evidence that the current institutional framework is not working for Scots.

Source: Modern Money Lab.

This time, the private balance is in black. Worth noting is that the level of household debt in the UK is around 75% of GDP at the moment (3Q 2025).

The private sector in the rest of the UK is able to net save twice as often as the private sector in Scotland.

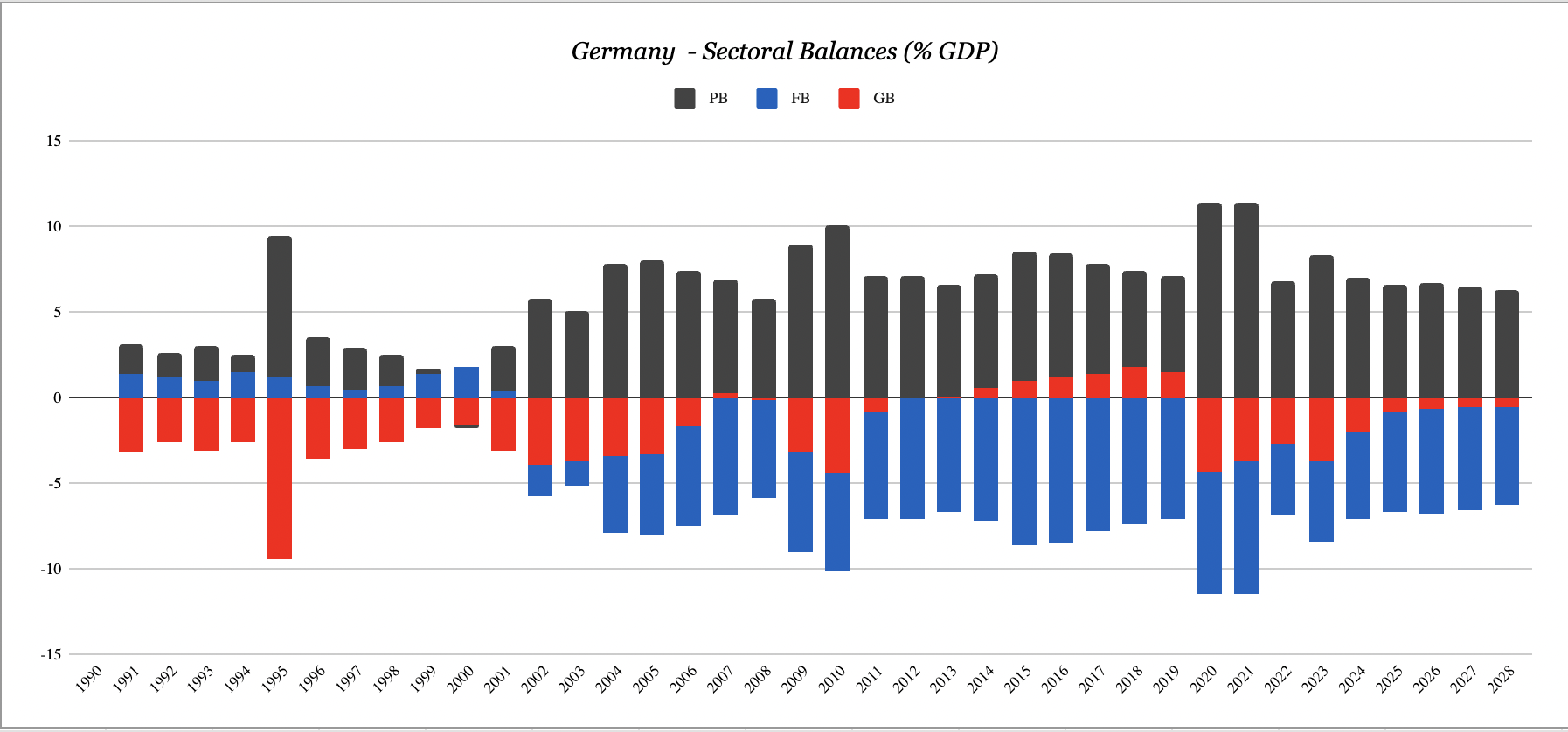

But even that level of saving is low compared to most other wealthy nations. Here are Germany’s sectoral balances.

Source: Modern Money Lab.

Once again, Private Balance is in Black. In 33 out of 34 years, the German private sector was able to net save. This puts the UK economy to shame. And not surprisingly, the household debt-to-GDP level is lower than in the UK, at under 50% of GDP.

The primary function of a government should be to ensure that, in most years, the private sector is able to net save.

But how often have you heard any government official say this?

Instead, they focus on ‘sound finance’, ‘sustainable public finances’. It is misdirection. And even worse, the continued focus on public debt will ensure a large financial contraction is on the horizon.

The UK public debt is not too high; it is too low.

Relative to the UK, the UK government spends too little in Scotland.

The obvious conclusion is that a new economic paradigm is needed. One that understands that all money is debt, but not all debt is the same. That government spending does not crowd out investment, it creates investment. And that the government deficit is the private sector surplus.

The current state of the UK means that the private sector across the UK is unable to save regularly. And it is even less often that this happens in Scotland. The neoliberal UK state drives financial fragility.